Issue: EXTROPY #16 · First Quarter 1996

Author: Duane Hewitt

Pages: 33–35 · 3 scanned pages

Idea Futures on the Web

Extropians may have previously encountered the Idea Futures (IF) concept either in the original paper by Robin Hanson [Extropy #8, 3:2, Winter 1991-2] or our paper and presentation for EXTRO². Idea Futures allows participants to make bets upon the likelihood of future events, called claims. For example, the purchase of a share in a claim at a price of 38 indicates the buyer believes there is a 38% or more probability of it coming true. The Idea Futures marketplace is basically a clearinghouse where individuals place bets upon various issues or even create markets in issues that interest them. The claim prices fluctuate depending upon the most current information related to the event.

The WWW Idea Futures market opened in September of 1994 with just ten players; over the past year the market has

grown to over 1500 participants and gained international recognition by winning The Golden Nica Award of the Prix Ars Electronica and more recently scoring in the top 5% in the Point Survey of Web sites. It has also received media coverage in Japan and Europe, and in Wired and the Los Angeles Daily News. It can be found on the Web at http://www.ideafutures.com/ Make sure to add it to your bookmarks file or hotlist.

How might an Idea Futures market change things?

Originally IF was envisioned as an alternative method to generate funding for scientific research. A real life example where IF could have been useful involves some controversy regarding the cause of stomach ulcers. Dr. Barry Marshall discovered a bacterium that he believed to be associated with ulcers in 1982. He had believed that a treatment with a standard antimicrobial regimen would be developed within a few years. However, this has not occurred. The association of the bacteria with ulcers has faced an uphill battle and the researcher even dosed himself with the bacterium to induce an ulcer and make his point. He was driven to this course of action by the refusal of the medical community to accept his research. As late as 1993 antacids used to treat ulcers without curing them were among the top selling drugs in the United States. Therefore there was a huge industry focused around treating the symptoms rather than curing the disease. Now

after over thirteen years an antimicrobial treatment is finally being developed.

If an Idea Futures market had been available at that time the following might have occurred. The researcher could have initiated, upon his discovery, an IF claim as follows:

” By January 1st, 1987 it will have been demonstrated that ulcers are caused by a bacterium and can be treated with antibiotics. ”

He could then have seeded the market with $2000 from his savings and put in bids that he would take bets at a 65% probability of this claim being judged true. The creation of the claim and the odds being offered are published in some journals that follow the Idea Futures market and in some medical journals

that track relevant claims. Some pharmaceutical companies with anti-ulcer medications coming through the approval pipeline and some biased skepticism drive the odds down to 0 by overwhelming the initial investment of the researcher. However, at this point the researcher has convinced a venture capitalist to back him and $50,000 is pumped into the market and the researcher is given some capital to continue his work. With this infusion of money the market odds rise to 45%. The companies decide to allocate enough money to push the odds down to 20% and they also allocate some funding for research to debunk the claims of the lone researcher.

The market’s capitalization creeps over the $200,000 threshold and starts to draw the attention of professional speculators.

Idea Futures on the Web

Duane Hewitt

The initial findings of the pharmaceutical companies contradict those of the researcher and the release of these results to the press results in the odds being driven down to around 10%. The lone researcher’s work has progressed and his results have been confirmed. He takes out a second mortgage on his house and puts $40,000 into the market. His actions do not go unnoticed as one professional speculator is having him tailed. Upon discovering the researcher’s investment the speculator deploys his resources and those of some of his clients in the market and then sells the information to other speculators. The market price climbs inexorably from 15% to around 80% with sudden surges in the price as people cancel booked orders until they can find out whether the information that the market is moving is sound. A press release of his latest results as well as that of some

35

EXTROPY #16 Q1 ‘96

independent researchers causes the market to move to 95% and he sells out all the shares that he has accumulated in the claim for over $400,000. He then uses this money to buy out his VC partner and to gear up his company for the delivery of this treatment. This capitalist fairy tale involves those who are correct being rewarded and those who are incorrect being penalized.

What is going on in the WWW Idea Futures market?

As in all markets there are buyers, sellers, commodities, prices and a currency. The buyers and sellers in the WWW Idea Futures market are the registered participants. (Free registration) Currently we are trading a proprietary currency called credibils that has no actual value outside the game. With this currency players may buy or sell the commodities in this market which are “coupons” in claims. Coupons are assets that have a value (price) that depends on the market consensus of the probability of the claim being judged. The value is quoted on the Transaction Form as creditcents (hundredths of a credibil). This value varies between 0 and 100 and can be read simply as the estimated probability of the claim coming true. Players may purchase a coupon that may either be a YES (the stated claim will come true) or a NO (the stated claim will not come true).

On the Table there are Bid and Ask prices for several claims from the IF market. Let us imagine that I am a firm believer that Cryonics is going to be a major growth industry in the next five years. I could then buy YES coupons in Cryo in anticipation of this growth meeting the criteria for the claim being judged true. One note of caution: the claim wording often is very important when estimating the probability of the claim being judged true or false. Therefore it is strongly recommended that the Long Description (separate Web page) be read carefully. I would have to pay the current Ask price if I wanted to make the transaction immediately. Therefore I would have to pay 0.14 credibils per Cryo YES coupon that I wished to purchase. If I wished to buy 100 YES coupons it would then cost me $14 (in credibils).

On the other hand, if I was skeptical about Cryonics catching on in the next

five years I could sell YES coupons short in the IF market. I would do so by selling YES coupons at the Bid price and since I don’t have any YES coupons to begin with what I will end up with is a negative number of YES coupons held which is the equivalent of holding NO coupons. (At this point I would strongly recommend the IF Web documentation and the IF tutorial by Ken Fishkin to further elucidate these concepts.) Another important thing to realize in dealing with NO coupons (negative YES coupons) is that the following formula applies:

(Ask Price of NO Coupon/100)+(Bid Price of YES coupon/100)= $1(credibil)

From this you can derive:

(Ask Price of NO coupon/100)= $1-(Bid Price of YES coupon/100)

In order to buy 100 Cryo NO coupons I would have to spend ($1-11/100) =$0.89 per coupon which ends up being 89 credibils. This brings to light one feature of the market—leverage. This allows people with unpopular or minority opinions a disproportionate effect on the market. In the Cryo claim we see that it takes $14 to purchase 100 YES coupons but requires $89 to purchase 100 NO coupons.

Idea Futures is a zero sum game in that the server processes the transactions for two parties and does not take any of the risk inherent to the wager. The winnings of one individual correspond to the losses of (an)other individual(s). Therefore the Idea Futures market can serve as a testing place for futurists, pundits, psychics and consultants in order to quantify their ability to make accurate predictions. This is currently reflected as the Score in the WWW market which is public.

Where do the prices come from?

In a market there are often people who are unwilling to pay more than a certain price for a commodity. Therefore there are often periods in which no activity occurs because nobody is willing to trade at the current price. In IF we have created a mechanism by which players can “book” orders at a specified price. What happens is that the individual places an order for a specific amount of

coupons at a specific price. This order is not executed until someone else is willing to make the complementary trade. Therefore every trade in IF involves one person who is logged on and completing someone’s booked order. The book is public and therefore you can see who is willing to buy coupons and at what price. This is a way to gauge the depth of the market in the claim.

What do the prices mean?

On the table the price for Cash is a Bid of 88 and an Ask of 89. Therefore there is a market consensus that there about an 88.5% chance that an electronic currency will be used for transactions before a specific date in 1997. The fact that the spread is only 1% indicates that there is a fairly strong consensus that the probability belongs in that range. Several other claims in the table share the characteristic of a very small spread. (Cr56, IDEA, Immo, Moon, Spce, SSTO, Stew, surg) This is very surprising for some of these claims because of the long time frames involved and the unpredictable nature of the advances required to make them possible. (eg. Immo, Moon, Stew) Some of these claims have larger spreads which indicates that the market estimates that they are more uncertain. (Canc, MLAW)

Some Observations from the market

Some interesting information can be gleaned from the market dynamics such as the estimated probability of the event (price), the uncertainty about the event’s probability (the spread) and the amount of interest in the issue (capitalization). The price is fairly straightforward in that it represents the estimated probability of the event occurring (as a percentage) and serves as the value of the coupons on the market. The spread, which is the difference between the Bid and Ask prices indicates how narrowly people are willing to pin down the probability of the claim coming true. The spread may be large because of uncertainty as to the exact probability of the claim coming true. This may be due to unclear claim wording or to uncertainties about the actual event. The capitalization indicates the credibil value of the outstanding coupons in the claim. It is a measure of the interest in this claim.

EXTROPY #16 Q1 ‘96

36

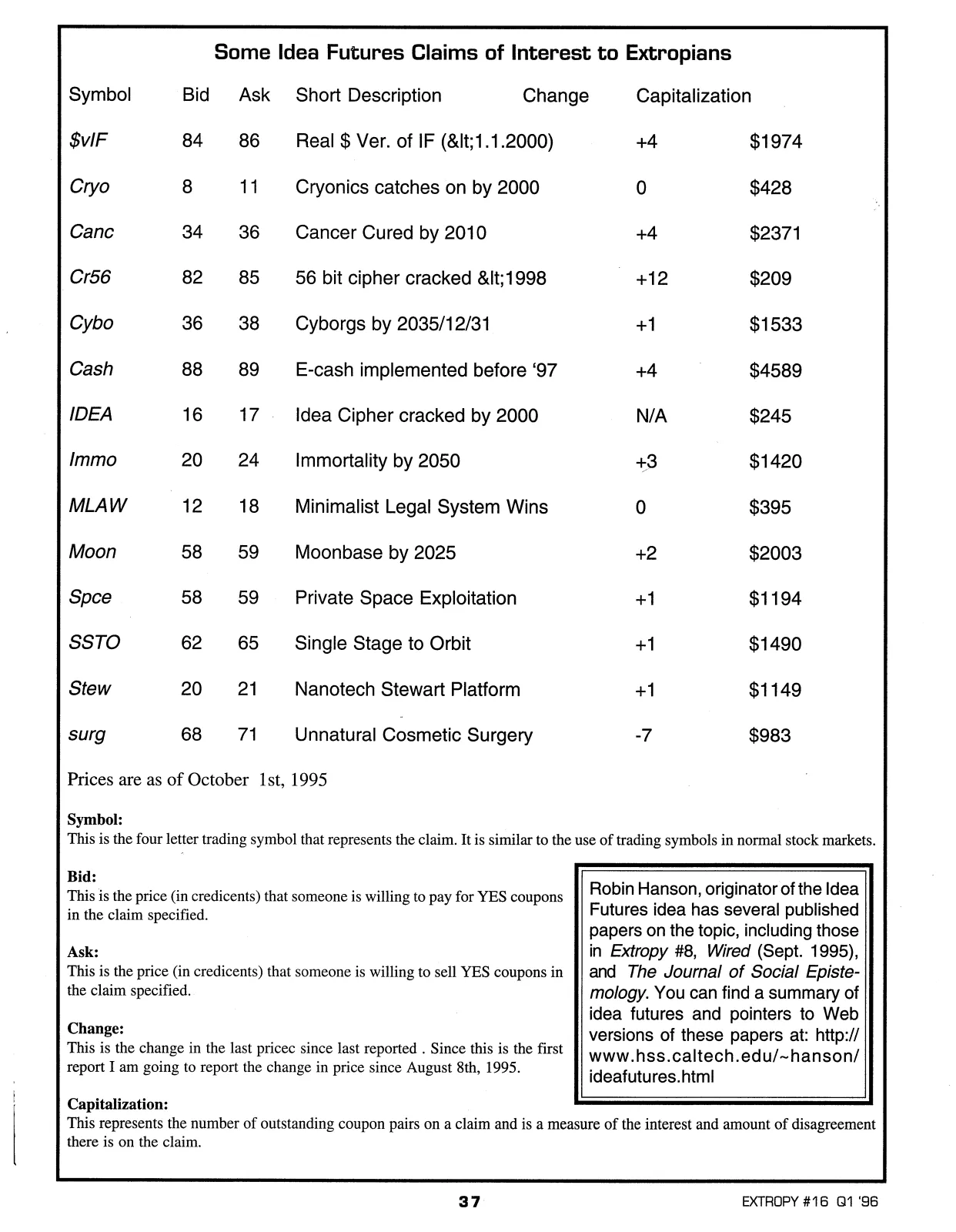

Some Idea Futures Claims of Interest to Extropians

| Symbol | Bid | Ask | Short Description | Change | Capitalization |

|---|---|---|---|---|---|

| $vIF | 84 | 86 | Real $ Ver. of IF (<1.1.2000) | +4 | $1974 |

| Cryo | 8 | 11 | Cryonics catches on by 2000 | 0 | $428 |

| Canc | 34 | 36 | Cancer Cured by 2010 | +4 | $2371 |

| Cr56 | 82 | 85 | 56 bit cipher cracked <1998 | +12 | $209 |

| Cybo | 36 | 38 | Cyborgs by 2035/12/31 | +1 | $1533 |

| Cash | 88 | 89 | E-cash implemented before ‘97 | +4 | $4589 |

| IDEA | 16 | 17 | Idea Cipher cracked by 2000 | N/A | $245 |

| Immo | 20 | 24 | Immortality by 2050 | +3 | $1420 |

| MLAW | 12 | 18 | Minimalist Legal System Wins | 0 | $395 |

| Moon | 58 | 59 | Moonbase by 2025 | +2 | $2003 |

| Spce | 58 | 59 | Private Space Exploitation | +1 | $1194 |

| SSTO | 62 | 65 | Single Stage to Orbit | +1 | $1490 |

| Stew | 20 | 21 | Nanotech Stewart Platform | +1 | $1149 |

| surg | 68 | 71 | Unnatural Cosmetic Surgery | -7 | $983 |

Prices are as of October 1st, 1995

Symbol:

This is the four letter trading symbol that represents the claim. It is similar to the use of trading symbols in normal stock markets.

Bid:

This is the price (in creditcents) that someone is willing to pay for YES coupons in the claim specified.

Ask:

This is the price (in creditcents) that someone is willing to sell YES coupons in the claim specified.

Change:

This is the change in the last price since last reported. Since this is the first report I am going to report the change in price since August 8th, 1995.

Capitalization:

This represents the number of outstanding coupon pairs on a claim and is a measure of the interest and amount of disagreement there is on the claim.

Robin Hanson, originator of the Idea Futures idea has several published papers on the topic, including those in Extropy #8, Wired (Sept. 1995), and The Journal of Social Epistemology. You can find a summary of idea futures and pointers to Web versions of these papers at: http://www.hss.caltech.edu/~hanson/ideafutures.html

37

EXTROPY #16 Q1 ‘96

VIEW ORIGINAL SCAN (3 pages)